Flexible Budget – Case of Redmond Management Association

Hello, and thank you for joining us for our flexible budgeting presentation. The focus of the talk will be on the non-profit Redmond Management Association’s flexible budget. In addition, the case study presentation will present a flexible budget for the firm, sales volume and variable cost volume variances, flexible volume variance, a justification for the variances, budget concerns for not-for-profit organizations, and budget concerns for not-for-profit organizations before making recommendations for Redmond Management Association regarding future luncheons.

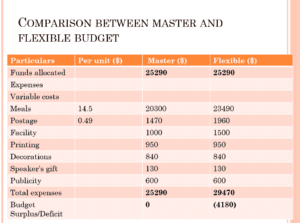

The comparison between the master and the flexible budget of Redmond Management Association is shown above. The master budget provides information planned by an organization. The flexible budget takes in the actual results, including the actual changes occurring during the financial period. A flexible budget, for example, is a financial instrument that is created after spending is classified into fixed, semi-variable, and variable categories (Warren & Jack, 2018). At various activity levels, the budget is utilized to determine costs, budgeted sales, and profits. Making a flexible budget allows managers to make a variety of decisions. For the subject luncheon, a deficit of 4180 is realized in the case of the Redmond Management Association. The company’s expenses exceeded the income generated for the luncheon in question, resulting in a deficit.

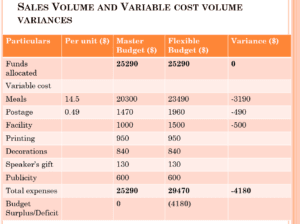

Variances are the differences between what an organization intends to spend in a certain financial period and what it actually spends on costs during that same time. Variable cost volume expenditures show the difference between budgeted and actual variable cost expenses, whereas sales volume expenses show the difference between budgeted and actual variable cost expenses (Nishimura, 2019). In the instance of the Redmond Management Association, the number of invites sent is interpreted as a measure of sales volume. This is especially true because the company is a non-profit organization. Variations in variable cost volume are shown in the table. They will, however, be addressed in greater depth in the section on variations.

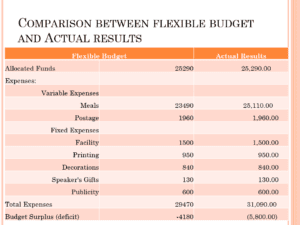

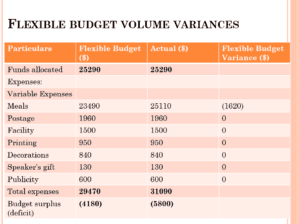

A comparison between the flexible budget and actual results is given in the table above. It indicates the budget deficit went higher from $4180 to $5800; thus, a concern is raised on why the flexible budget did not factor in the possible changes in the operations of the company. However, the reasons why the variances occurred are given towards the end of our presentation. Notably, the difference between the flexible budget outlay and the actual result occurred due to the increased number of meals.

The calculations for variances are shown in the table above, which are based on a comparison of the flexible and actual budgets. Only for meals is a flexible volume variance achieved, in which more meals were consumed than the flexible budget for meals planned. On the other hand, all other costs were evenly distributed between the flexible and actual budgets, resulting in a variance value of zero. This is because the Redmond Management Association was able to stay within its established parameters.

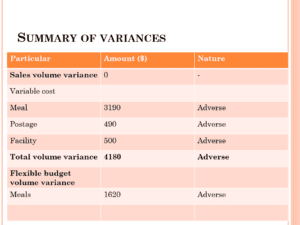

The table above is a summary of the deviations. It has a framework for flexible budget volume variations and variable cost volume variances. To begin with, the variance in sales volume is 0 because no sales were made. There were $3190 in food differences, $490 in mail disparities, and $500 in facility variances due to variable cost anomalies. All three are negative variances, resulting in a total volume negative variance of $4180. This indicates that the Redmond Management Association spent $4180 more than the budgeted amount. The flexible budget volume variance, on the other hand, suggests a $1620 variance, which is likewise negative. It also signifies that the corporation spent $1620 more than the budgeted amount.

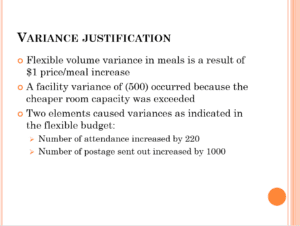

The Redmond Management Association variations indicated in the preceding sections happened for various reasons. First, attendance climbed by 220 people, exceeding the firm’s expectations. Second, the amount of postage that was sent out rose by 1000. The lower room capacity in which the luncheon was held justifies the negative variation in facilities stated in the preceding section. The capacity was surpassed by 500 people. In the preceding sections, there existed a flexible volume variance that might be justified by a $1 increase in the price of each meal.

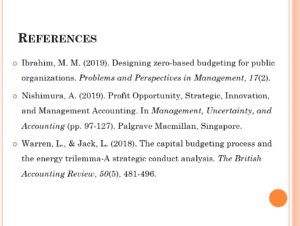

According to this presentation, not-for-profit groups like the Redmond Management Association are concerned about budgets despite their charitable status. For starting, budgeting is important to such companies since it may help them maintain their activities for a long period. Notably, both profit-making and non-profit organizations want to be sustainable for extended periods. Second, non-profit organizations keep budgets to guarantee that present and future income flows are not disrupted. Third, budgeting is a critical tool for keeping track of an organization’s success. Budgeting, for example, tells businesses if they are on track to accomplish their goals and, if not, how far behind they are. Finally, for-profit and non-profit organizations have resources that must be efficiently utilized (Ibrahim, 2019). Budgeting ensures that resources are used efficiently; thus, not-for-profit organizations should be concerned with budgeting.

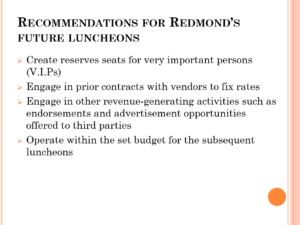

The Redmond Management Association can implement a variety of proposals depending on the flexible budgets developed. First and foremost, the Redmond Management Association should consider adding seats that generate more revenue than the present ones. The company should consider purchasing seats for very important people (V.I.P.) at a greater cost. Second, the organization should consider engaging in earlier contracts, such as future contracts, to determine the amount of revenue they are anticipated to generate in order to avoid unprecedented deficits. Third, the Redmond Management Association should think about diversifying its revenue streams by participating in other activities. To create extra cash, they may, for example, engage in marketing and endorsement activities for other firms. Finally, the organization should ensure that it operates within its budget to minimize financial deficits.

The Redmond Management Association can implement a variety of proposals depending on the flexible budgets developed. First and foremost, the Redmond Management Association should consider adding seats that generate more revenue than the present ones. The company should consider purchasing seats for very important people (V.I.P.) at a greater cost. Second, the organization should consider engaging in earlier contracts, such as future contracts, to determine the amount of revenue they are anticipated to generate in order to avoid unprecedented deficits. Third, the Redmond Management Association should think about diversifying its revenue streams by participating in other activities. To create extra cash, they may, for example, engage in marketing and endorsement activities for other firms. Finally, the organization should ensure that it operates within its budget to minimize financial deficits.

ORDER A PLAGIARISM-FREE PAPER HERE

We’ll write everything from scratch

Question

Flexible Budget – Case of Redmond Management Association

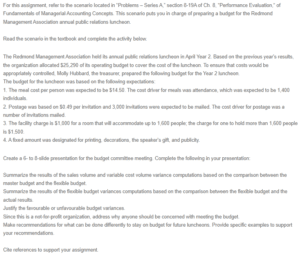

For this assignment, refer to the scenario located in “Problems – Series A,” section 8-19A of Ch. 8, “Performance Evaluation,“ of Fundamentals of Managerial Accounting Concepts. This scenario puts you in charge of preparing a budget for the Redmond Management Association annual public relations luncheon.

Read the scenario in the textbook and complete the activity below.

The Redmond Management Association held its annual public relations luncheon in April Year 2. Based on the previous year’s results, the organization allocated $25,290 of its operating budget to cover the cost of the luncheon. To ensure that costs would be appropriately controlled, Molly Hubbard, the treasurer, prepared the following budget for the Year 2 luncheon.

The budget for the luncheon was based on the following expectations:

1. The meal cost per person was expected to be $14.50. The cost driver for meals was attendance, which was expected to be 1,400 individuals.

2. Postage was based on $0.49 per invitation and 3,000 invitations were expected to be mailed. The cost driver for postage was a number of invitations mailed.

3. The facility charge is $1,000 for a room that will accommodate up to 1,600 people; the charge for one to hold more than 1,600 people is $1,500.

4. A fixed amount was designated for printing, decorations, the speaker’s gift, and publicity.

Create a 6- to 8-slide presentation for the budget committee meeting. Complete the following in your presentation:

Summarize the results of the sales volume and variable cost volume variance computations based on the comparison between the master budget and the flexible budget.

Summarize the results of the flexible budget variances computations based on the comparison between the flexible budget and the actual results.

Justify the favourable or unfavourable budget variances.

Since this is a not-for-profit organization, address why anyone should be concerned with meeting the budget.

Make recommendations for what can be done differently to stay on budget for future luncheons. Provide specific examples to support your recommendations.

Cite references to support your assignment.