Accounting Cycle and Financial Reporting

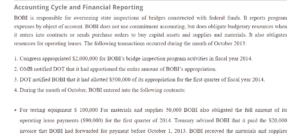

IN THE BOOKS OF BOBI |

||||||||

JOURNAL ENTRY |

||||||||

| BUDGETARY ACCOUNTS | PROPRIETARY ACCOUNTS | |||||||

| Sl. No. | Particulars | Debit | Credit | Sl. No. | Particulars | Debit | Credit | |

| 1) | Appropriations realized A/c… Dr | $ 2,000,000.00 | 1) | No entry | ||||

| To Unapportioned authority | $ 2,000,000.00 | |||||||

| 2) | Unapportioned Authority A/c…Dr | $ 2,000,000.00 | 2) | No entry | ||||

| To Apportionments | $ 2,000,000.00 | |||||||

| 3) | Apportionments A/c. Dr | $ 500,000.00 | 3) | Fund balance with treasury A/c. Dr | $ 500,000.00 | |||

| To Allotments | $ 500,000.00 | To capital appropriations | $ 500,000.00 | |||||

| 4) | Allotments Ac..Dr | $ 240,000.00 | 4) | No entry | ||||

| To Obligations-undelivered orders | $ 240,000.00 | |||||||

| 5) | Obligations-undelivered orders A/c. Dr | $ 20,000.00 | 5) | Operating expenses A/c Dr | $ 20,000.00 | |||

| To Expended Appropriations | $ 20,000.00 | To fund balance with treasury account | $ 20,000.00 | |||||

| 6) | Allotments Ac..Dr | $ 2,000.00 | 6) | Material and supplies A/c..Dr | $ 52,000.00 | |||

| Obligations-undelivered orders A/c. Dr | $ 140,000.00 | Operating expenses A/c Dr | $ 30,000.00 | |||||

| To Expended Appropriations | $ 142,000.00 | To Accounts payable | $ 82,000.00 | |||||

| 7) | No entry | 7) | Accounts Payable A/c. Dr | $ 82,000.00 | ||||

| To Disbursement in transit | $ 82,000.00 | |||||||

| 8) | No entry | 8) | Salaries A/c. Dr | $ 90,000.00 | ||||

| To Disbursement in transit | $ 90,000.00 | |||||||

| 9) | Allotments Ac..Dr | $ 172,000.00 | 9) | Disbursement in transit A/c..Dr | $ 172,000.00 | |||

| To Expended Appropriations | $ 172,000.00 | To fund balance with treasury account | $ 172,000.00 | |||||

| 10) | No entry | 10) | Salaries A/c. Dr | $ 10,000.00 | ||||

| To Salaries payable A/c | $ 10,000.00 | |||||||

| Materials consumed | $ 12,000.00 | |||||||

| To material and supply A/c | $ 12,000.00 | |||||||

| Depreciation A/c Dr. | $ 1,000.00 | |||||||

| To Accumulated Depreciation on Equipment | $ 1,000.00 | |||||||

| b) |

Preclosing Trial balance |

|||||||

| Budgetary accounts: | ||||||||

| Appropriations realized | $ 434,000.00 | |||||||

| Delivered order-obligations unpaid | $ 100,000.00 | |||||||

| Expended Appropriations | $ 334,000.00 | |||||||

| c) | BALANCE SHEET | |||||||

| Assets | ||||||||

| Fund balance with treasure | $ 328,000.00 | |||||||

| inventory, material, and supplies | $ 46,000.00 | |||||||

| General property, plants, and equipment | $ 30,000.00 | |||||||

| Less: Accumulated Depreciation on Equipment | $ (1,000.00) | $ 29,000.00 | ||||||

| Total Assets | $ 403,000.00 | |||||||

| Liabilities | ||||||||

| Disbursement in transit | $ 20,000.00 | |||||||

| Accounts payable | $ – | |||||||

| Salaries Payable | $ 10,000.00 | |||||||

| Cumulative results of operation | $ 373,000.00 | |||||||

| Total liabilities | $ 403,000.00 | |||||||

Other Related Post: https://eminencepapers.com/create-a-budget-and-financial-plan-for-a-vacation-trip/

ORDER A PLAGIARISM-FREE PAPER HERE

We’ll write everything from scratch

Question

Accounting Cycle and Financial Reporting

BOBI is responsible for overseeing state inspections of bridges constructed with federal funds. It reports program expenses by the object of account. BOBI does not use commitment accounting but obligates budgetary resources when it enters into contracts or sends purchase orders to buy capital assets, supplies, and materials. It also binds resources for operating leases. The following transactions occurred in October 2013:

Accounting Cycle and Financial Reporting

- Congress appropriated $2,000,000 for BOBI’s bridge inspection program activities in fiscal year 2014.

- OMB notified DOT that it had apportioned the entire amount of BOBI’s appropriation.

- DOT notified BOBI that it had allotted $500,000 of its appropriation for the first quarter of fiscal year 2014.

- During October, BOBI entered into the following contracts:

- For testing equipment, $ 100,000. For materials and supplies, 50,000 BOBI also obligated the total amount of its operating lease payments ($90,000) for the first quarter of 2014. Treasury advised BOBI that it paid the $20,000 invoice that BOBI had forwarded for payment before October 1, 2013. BOBI received the materials and supplies ordered in transaction 4. However, the invoice was for $52,000 because the supplier sent additional supplies, as permitted by the contract. BOBI accepted the entire shipment. BOBI also recorded as a liability the $30,000 rent due October 1. BOBI sent a disbursement schedule to Treasury requesting the following payments: For materials and supplies, $ 52,000 For rent 30,000; BOBI sent a disbursement schedule to Treasury asking for salary checks totaling $90,000. Treasury advised BOBI that it had made payments totaling $172,000 under the programs forwarded by BOBI in transactions 7 and 8. To prepare accrual-basis financial statements for October, BOBI made adjusting journal entries for the following items: To accrue salaries earned in October but not paid—$10,000 To record materials and supplies used—$12,000 To record one month’s depreciation on equipment—$1,000

Use the preceding information to do the following:

- Prepare journal entries to record the initial transactions and events.

- Prepare a preclosing trial balance based on the transaction

- Prepare a balance sheet, a statement of net costs, and a notice of changes in net position.